NH CIBIL Score! How to generate CIBIL score first time?

Are you facing loan rejections because of your NH CIBIL score? If you’re new to the credit world, it can be difficult to avail an unsecured loan, especially when you’re applying for a big-ticket loan like a home loan, personal loan, or business loan. Bank managers often expect a solid credit history before approving such applications. In this scenario, you should focus on building your credit score first. A good credit history not only improves the chances of getting a big-ticket loan approval but also helps you secure better interest rates and preferred loan terms that ultimately saves a lot of money in the long run. Today, in this blog, we will learn how to generate CIBIL score first time and how to maintain it. So, let’s start the discussion with the basic understanding of the NH CIBIL score.

What is NH CIBIL score?

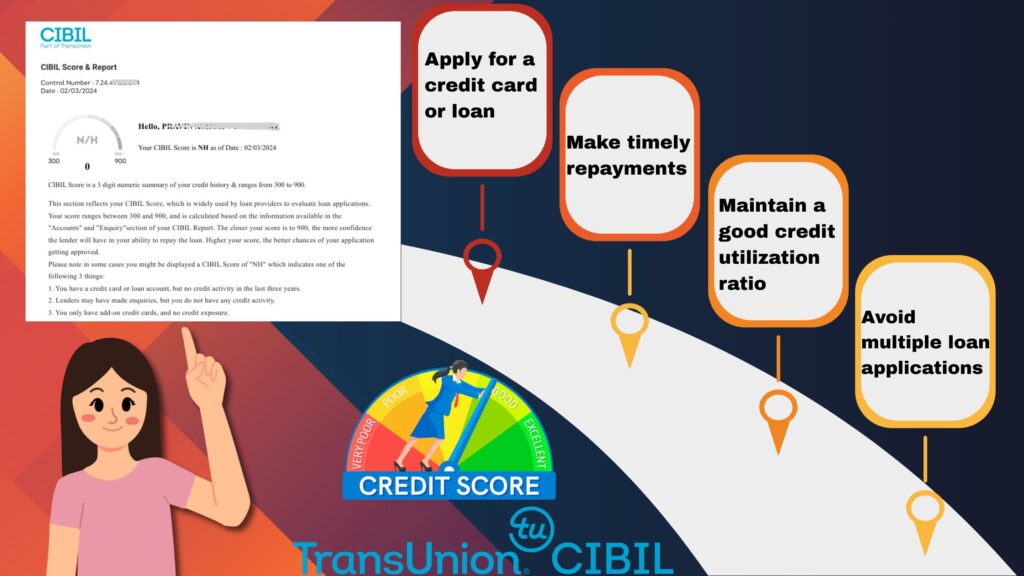

The terminology “NH” in CIBIL score means No Credit History. It indicates that the individual does not avail of any credit facility, or he has had no credit activity for the last couple of years.

Typically, when an individual avails a loan or any other credit facility from a financial institution, they report the particular borrower’s credit information and loan repayment records to all the credit information companies, including TransUnion CIBIL. Based on the credit behaviour and loan repayment pattern, TransUnion CIBIL evaluates a unique credit score for the particular customer, ranging between 300- 900.

Now, if you have not taken any loan, credit cards, or any other credit line yet, in that case, the respective credit bureau doesn’t have enough information to compute a credit score for you. As a result, you will find “NH” or “-1” CIBIL score in your credit report. Due to this absence of credit history, bank managers face problem to access your creditworthiness and sometimes, it’s viewed negatively in case of a big-ticket loan approval.

That’s why, if you are a first-time borrower and facing difficulties to secure a large amount of loan or premium credit card approval, start your credit journey with a small ticket loan or entry-level credit cards. So, let’s discuss about the most effective techniques to build your CIBIL score from scratch.

The most effective ways to generate CIBIL score first time:

• Gold loan:

Taking out a gold loan is one of the most convenient and easy ways to start your credit journey. It is a secured loan, where you pledge your gold as collateral, whether in the form of jewellery, coins, or gold bars. Since you’re receiving money in exchange for your gold, banks typically do not focus on your credit score. Gold loans also come with quick approvals and lower interest rates that make it affordable to repay smoothly.

So, start with a small amount of gold loan and pay it regularly. Once the respective lender reports the gold loan account to the credit bureau, your CIBIL score will be generated automatically.

• Secured credit card:

If you don’t have enough gold, you can opt for a secured credit card. A secured credit card offers low-risk access to credit, where the card is backed by a fixed deposit. The credit card limit is usually linked to the FD amount, where most banks offer 75 to 90% of the deposited value. Due to this security, it is relatively easy to get approved, even with an NH CIBIL score.

Credit cards typically come with high interest rates, so it’s important to compare different credit cards and choose the one that suits you best. Additionally, when using secured credit cards, make sure to pay your bills on time and maintain a low credit utilisation (ideally below 30% of the credit limit) to build a strong credit history.

• Buy-now-pay-later service:

In today’s financial market, Buy Now Pay Later (BNPL) services have become a popular trend among consumers. This user-friendly option allows customers to purchase goods or services without any upfront payment and pay them back in instalments.

Many well-known e-commerce platforms (such as Flipkart and Amazon) and online payment gateways (like Paytm, Flexipay, and Lazypay) offer such pay-later services to their customers.

When you avail of any pay-later service, it is treated as a credit facility and reported to your credit report. By opting for such an effective tool, you can generate your credit profile and build a strong credit history.

• Consumer durable loan:

If you’re completely new to credit, then consumer loans can be an easy-to-access product for you. It is a quite popular loan segment, which requires minimal documentation. You can purchase your household products and electronic appliances on EMIs. When you pay the loan EMIs timely, it will help to build a strong repayment track.

• Instant personal loan:

If a bank manager refuses to approve a large personal loan, you can initially approach them for a small-ticket loan. Since the risk is lower, they may be willing to accept your NH CIBIL score.

In addition, in today’s digital age, many loan apps offer online instant loans with minimal documentation, even for individuals with no credit history. By taking out such short-term loans and repaying them on time, you can build your CIBIL score and demonstrate responsible credit behaviour.

However, be cautious as these online instant loans often come with high-interest rates. It’s essential to compare different options, thoroughly read the terms and conditions, and choose a reliable and trustworthy lender.

• Apply for a loan or credit card from the same bank where you have an account:

Whether you’re a salaried or self-employed individual, you must have a savings account or a current account. In case other banks deny your loan or credit card application, you can approach your own bank. Since they have access to your complete financial history and transaction details, they are more likely to consider your no-credit history (NH CIBIL score) and approve your loan based on the financial relationship you have built with them. This can make it easier to secure loan approval.

• Addon card holder:

If you are a young individual with no prior credit history, becoming an authorised user on someone else’s credit card can help you build your credit profile quickly. This person can be a close family member, such as a parent, sibling, or even a trusted friend.

As an authorised user, the credit card account will also be reported on your CIBIL report. When the primary account holder uses the card responsibly and makes timely payments, their strong repayment history will positively reflect on your credit report as well.

However, be cautious—if the primary account holder defaults on payments, it can negatively affect your CIBIL score too. Therefore, consider this option carefully and preferably keep it as a last choice.

• Pre-approved loan:

If you are a salaried individual, you may often receive pre-approved loan offers from various lenders. Some lenders may even be willing to accept your NH CIBIL score. However, make sure to carefully review all terms, conditions, and fees before applying.

How much time does it take to generate CIBIL Score First Time?

Building your credit score from scratch is not an overnight process. When you avail a new credit facility, it typically takes around 15-30 days for the loan account to be reported in your CIBIL report. Once the account appears, a CIBIL score is generated automatically based on the credit bureau’s internal scoring algorithm. As you continue to pay your loan dues on time and use credit responsibly over a period of 3-6 months, your score will gradually improve. That’s all about, how to generate CIBIL score first time. Now, it’s your turn to start your credit journey.