A home is a dream for every individual in our country.It is something that everyone desires and has plans or ideas for their dream home.So to make it a reality everyone has to make a full proof plan to execute the whole process of owning a house. Punjab National Bank or PNB has come up with various kinds of home loan products for every individual. So before going for a plan to possess a dream home every applicant must check the PNB home loan eligibility of their own to make the dream come true.

Forewords to PNB home loan eligibility

In the previous days the price of land was comparatively lesser, where a person would work and save money to pay the full amount for a house without taking any loan.

But nowadays, the cost of houses is so high that not many can pay the full cost of a house without home loans from banks like Punjab National Bank and to make the whole plan a successful one it is always advisable to check the various kinds of PNB home loan products.

These PNB home loan products have been designed so fantastically that it will definitely suit the PNB home loan eligibility criteria of all the individuals based on their profile.

Government initiatives: The Government has also taken initiatives understanding that the cost of homes and the loan taken is a long-term liability so to make it beneficial for the borrower it has provided tax benefits and subsidized housing through schemes like PMAY which makes housing affordable.

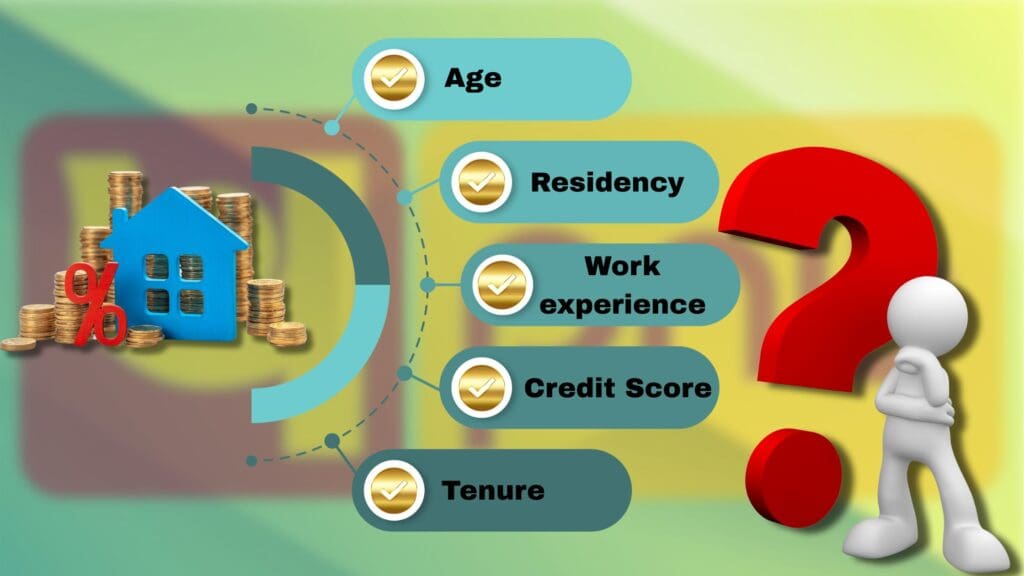

PNB Home Loan Eligibility Criteria:

PNB home loaneligibility depends on some criteria which are very flexible and easy for an applicant to get fulfilled while applying for a home loan.

There are certain factors or criteria stipulated by the public sector banks like PNB which need to be satisfied before loan applications are approved. They are as follows:

Profile Criteria Salaried and Self-Employed

Income Criteria Minimum salary for Punjab National Bank (PNB) Home Loan Rs.25000

Age Criteria 21 years to 70 years from the beginning of the loan tenure till it ends

Credit score A minimum credit score of 650 is required

Work Experience 3 years of complete work experience or business continuity is required.

Nationality Resident and Non Resident Indian

Home loans should be considered an investment by the borrower and that happens for a long term and a huge amount is invested on an individual with the guarantee he or she will pay back the home loan with interest.

This is the reason why banks like Punjab National Bank (PNB) have flexible PNB home loan eligibility criteria to make sure they are providing funds to the right person and to make sure that the person does not feel burdened in paying their home loan EMI and not have enough funds for their daily expenses.

Credit Score and Credit Report

Being a home loan applicant one must check his or her credit score before applying as this is a vital criterion for PNB home loan eligibility. For home loan eligibility the credit score of an applicant should be at least 650 as per Transunion CIBIL.

A credit report is one that along with the credit score it keeps the track of the credit accounts while giving a view of the complete history with credit via past accounts, past payments and the eligibility.

But the credit report must be free from the status like “settled” or “written off” etc. Any bank, when it gets a loan or credit card application will pull out the individual’s credit score or credit report which is available with the number of credit bureaus like CIBIL Part of Transunion, Equifax, Experian and Crif High Mark operating in the country.

The credit score is the accumulated score based on how regular the borrowers were in paying back the existing loans or credit card bills. This is the very first step taken by Punjab National Bank to set the PNB home loan eligibility criteria while screening the application. If the credit score is too low, then there is a good chance that your loan might be rejected.

Can late payment in the credit report hamper the home loan eligibility?

A credit report contains the complete history of the loans availed and utilized by the applicants along with the track record of how regularly they were paid.

The credit report shows every minute payment irregularities with complete details like late payments if any etc. If any applicant has the terms “settled” or “written off” against any credit account in the past, the home loan eligibility will be hampered and the application will be rejected as these terms indicate that the applicants have defaulted the loans and that the lender has settled the account realizing that the individual will not pay back the balance.

Similarly, if there are any discrepancies like mismatch of date of birth from what is on the application then it is grounds for rejection of Home loan. So it is always best to rectify any such discrepancies well in advance to meet the PNB home loan eligibility criteria so that the application is accepted successfully.

Home Loan Eligibility Check For Variant Home Loans:

PNB home loan eligibility criteria for variant home loansare based on minimal criteria depended on income or salary which makes it accessible to a wide range of individuals. The maximum repayment tenure is 30 years with attractive interest rates starting from 8.15% per annum.

PNB home loan products are suitable to individuals who have a regular source of income, i.e., who are salaried, self-employed, professionals, farmers, entrepreneurs, etc. It is also open to staff members of the bank.

PNB home loan eligibility for product like Flexible Housing Loan, the maximum age for eligibility is 60 years for applying and it is provided till the age of 70 years.

For the PNB Gen-Next Housing Finance Scheme, the maximum age for eligibility is 50 years, with a minimum net monthly income of Rs.35,000, and minimum 3 years of experience. This scheme is for employees of the state or central government, Public Sector Undertakings (PSUs), public sector banks, as well as those in the IT industry.

PNB home loan is provided for the following purposes:

For construction of house or flat;

For purchase of a built house or flat.

For purchase of an under construction house/flat from Housing Boards or Development Authorities or Co-operative Societies or Approved Private Builders or Projects.

For carrying out Additions to the house/flat.

For carrying out repairs or renovation or alterations or cost of furnishing to the house or flat.

For meeting cost escalation in the cases of under-construction flats to existing Housing Loan borrowers.

For purchase of land or plot for house building.

For PNB home loan eligibility for products like Housing Finance Scheme For Public – PNB Max-Saver the objectives are as follows:

This variant provides the borrowers advantage of substantial savings on the interest component on account of facility to:

Deposit their surplus funds in the overdraft account; and withdraw the same (up to the drawing power) at their choice as per their needs.

PNB home loan eligibility for products like Housing Finance Scheme For Public-PNB Max-Saver

Prospective borrower – As per our existing housing loan scheme.

Existing borrower – Where complete disbursement has been made.

The existing Housing Loan borrower desirous of availing loan under the variant be allowed the benefit provided their Housing Loan account is running regular, no outstanding inspection irregularity, complete disbursement has been made & repayment has started in the account.

PNB home loan eligibility criteria for products like Housing Loan for Public – Pradhan Mantri Awas Yojana – Housing for All are ensured based on the availability of Housing Loan to Individuals from Economically Weaker Section (EWS) &Low Income Group (LIG) category at attractive rates and ensure a house for all.

PNB home loan eligibility criteria for products like Pride Housing Loan For Government Employees the home loan product ensures availability of Housing Loan at attractive rates and ensures a house for all government employees.

All Central or State Government Employees or Defence personnel or Para military Forces & Pensioners of Central & State Government. Concessional rate of interest, irrespective of CIC score. Full waiver of upfront/ processing fees & documentation charges.

Before a person applies for PNB home loan products it is best to do a PNB home loan eligibility check which is available on the Punjab National Bank (PNB) website. This way the credit score will not be affected as the bank will only soft pull the credit score and compare it with other internal criteria to make sure that the applicants are eligible or not.

What are the reasons which might result to PNB home loan application rejected?

Required income from salary or self-employment:

Income from salary or income from business or profession is a very important criterion for a home loan. If the applicant or applicants does not match the PNB home loan eligibility criteria stipulated by Punjab National Bank (PNB) the application for PNB home loan products may be rejected.

There is also the other scenario where though the applicants have higher income the application might also get rejected because of lower disposable income which might not satisfy the loan EMI to income ratio also known as FOIR (Fixed Obligation to Income ratio). This means that the applicant does not have enough income in hand after paying the monthly EMI.

Stable job or business and profession:

If you are applying for a home loan immediately after joining a new job your application will be rejected. Banks expect any home loan applicant to be in a stable job, which will not be the case if you are new to the company which in turn means you are a risk. It is best to wait at least 6 months to a year in the new job before applying for a home loan.

List of approved employers and positive business profile:

The applicant might be working in a company or running a business or profession which is not in the list of approved employers or the profile of the business is negative to the banks. In such cases the banks feel that the job or business and profession of the applicants is not secure and not reliable to pay back the loan amount. It is very important to know whether the bank that has the company listed or the business profile positive will make sure that the application for PNB home loan eligibility criteria is met with good terms and not rejected

The property has legal problem:

When applying for PNB home loan products all the original documents pertaining to the property must be submitted to Punjab National Bank (PNB) for PNB home loan eligibility. This is because the property acts as the collateral for the home loan. If there is not proper documentation or if the property is under some legal litigations, then the home loan will be rejected.

As a precaution it is best to verify all the documents and property details before purchasing. The applicant can also visit the sub-registrar’s office or the corporation, muipality, zilla parishad or panchayatas per the applicability to make sure there is no problem with the property legally or if it falls under any Government plan.

Co-applicant has poor credit score:

In today’s scenario most home loan applicants go for joint applications to reduce the burden of EMI. Even though taking a joint home loan has its own advantage it can also be a cause for the application to be rejected if your co-borrower’s credit score is low.

This is because the loan amount and EMI will be decided based on the combined profile of all the applicants. So, if one applicant has a low credit score it will bring down the overall score of the group.

High level of debt or is already a loan guarantor:

Home loans being a high value investment, also means that the EMI each month will be high. If an applicant already has debts that need to be repaid, then the loan application might be rejected.

Similarly, if the applicant is already acting as a guarantor for another loan, then there is a risk that the other person might not pay their loan and will fall on the applicant who will have to pay the dues as a guarantor. This is also a reason for the application for PNB home loan products getting rejected.

Frequent enquiries for home loans:

If a person applies for home loan multiple times within a very short period, it will create an impression that the applicant or applicants does not manage finances properly and are always looking for credit and has the tendencies for over spending. This shows the bank that the borrowers are unreliable, and the PNB home loan eligibility criteria is not matched thus resulting to rejection of application.

Frequently asked questions:

1.How can I increase my PNB home loan eligibility?

You can increase your PNB home loan eligibility by adding a co-applicant who can be a parent, spouse, or children who are drawing a regular salary or have a stable source of income. The co-applicant should also be made the co-borrower of the home loan.

2. How much loan will I be eligible for under Punjab National Bank home loans?

The quantum of loan you will be eligible for under PNB home loan eligibility criteria will depend on your income and repayment capacity and is need- based depending on the cost of property as well.

3. Am I eligible for a moratorium for PNB home loans?

Yes, PNB home loan eligibility criteria includes moratorium which will depend on the nature of property, i.e., for a ready-built house or flat or plot of land the moratorium is for 3 months or till possession date, whichever is earlier, while for construction of a house or flat, the moratorium is for 18 months or till the project is complete, whichever is earlier.