When it comes to major expenses such as buying a home, purchasing a new car, renovating a property, planning a wedding, or handling medical emergencies, most of us rely on loans to meet our financial needs. But what if your loan application gets rejected due to a “written off” status in your CIBIL report? Typically, a “written off” status in a loan account indicates that the particular credit facility has been classified as an uncollectible debt by the lender. It suspects that you’re a loan defaulter and not a trustworthy borrower for future credit. In this situation, you should rectify the written off in CIBIL and rebuild your credit score first, before doing any further applications.

This article will provide a detailed discussion on the reasons of reporting a “written off” status, the procedure to rectify the negative mark, and the RBI’s new guidelines on written off in CIBIL report. Let’s begin with a basic understanding of the “written off” status in a loan account.

What is the meaning of written off status in CIBIL Report?

In the banking sector, loan write-off is a procedure of declassifying bad assets from the balance sheet. In general, when you avail of a credit facility from any back, obviously, it’s a liability for you. But from the bank’s perspective, it is considered an asset.

As long as you serve the loan interest, they make profits out of it. Now, in case you fail to repay your loan for three consecutive months, then the loan will turn into an NPA (Non-Performing Asset).

Bank always gives you opportunities to pay back the unpaid due. However, if you continue to default for 6-12 months, after a point, the bank eliminates such NPA or bad assets from their books of account. In accounting terminology, this procedure is known as “Write-off”.

When a lender writes off your unpaid debt, they simultaneously report the loan account as “Written-off” to all Credit Information Companies, including TransUnion CIBIL. As a result, you’ll find the “written-off” status in your CIBIL report, which severely impacts your CIBIL score and makes you ineligible for further loan approvals.

It’s important to remember that writing off a loan does not mean the lender forgives the outstanding amount. You are still obligated to repay the loan. In fact, the lender may also initiate legal action to collect the unpaid debt.

Different reasons of reporting written off in CIBIL:

There can be several reasons of reporting written off status in a CIBIL report. Obviously, it’s the borrower’s fault, but sometimes, a “Written-off” status can be mentioned in CIBIL report due to the negligence of the lender and some technical issue of the credit bureau. Let’s explain how.

● Written off status in an unknown loan account:

Let’s imagine this situation: As a responsible borrower, you always meet your obligations. But when you apply for a new loan, the bank manager rejects your application, by saying there is a written off in your CIBIL report. Upon investigation, you discover that the delinquent account is completely unknown to you. It’s frustrating, right?

Basically, this kind of issue arises when your Name, DOB, Address and other identification details are quite similar to an unknown loan defaulter. Due to these similarities, someone else’s written-off loan can mistakenly appear in your CIBIL report.

However, there’s no need to panic. In this case, you can remove the entire written off loan account from your CIBIL report by raising your concern to CIBIL customer care authorities. After verification, they will remove the account from your credit report and you will get back your CIBIL score as previous.

● Written off in CIBIL due to non-updation:

In some cases, even if you have paid off the entire loan outstanding, it may still show as ‘Written Off’ in your CIBIL report because the lender failed to update the loan properly. This usually occurs due to negligence or miscommunication between the lender and the credit bureau. In such cases, you need to follow up with both the lender and the respective credit bureau until your report gets rectified.

● Written off in CIBIL due to non-payment:

This is the case where you have defaulted on your ongoing loan for an extended period and have not cleared the dues yet. In this situation, you simply need to pay the outstanding loan balance and raise your concern with CIBIL authorities to have your CIBIL report rectified.

● Written-off in a settled loan:

This is a special case where a Written-Off status appears on a previously settled loan account. Technically, when you settle a written-off loan, it should be reported as Post Write-Off Settled in your CIBIL report. However, some PSU banks and private lenders keep the loan status as “Written-off”, as they made a loss here.

To rectify this, you may need to pay the remaining outstanding amount or the loss-on-closure amount. Once cleared, the lender should update your CIBIL report accordingly.

Process to rectify written off in CIBIL report:

● Contact with the lender:

To rectify the Written-off status in your CIBIL report, first, you should contact the respective lender. You can reach them by sending an email or visiting the loan-availing branch. Ask them to share the entire loan outstanding amount or the loan account statement. Try to collect all the payment details in written format.

● Pay the outstanding balance and collect the No Dues Certificate:

Now, after getting the payable amount details pay the same amount as per the lender’s demand. Don’t forget to collect the No Dues Certificate from them, as it will act as evidence when you raise further complaints in CIBIL. Be assured, in terms of payment; don’t go for any kind of settlement as it will impact negatively on your CIBIL Report.

● Raise dispute in CIBIL:

Now, it’s time to raise your concern to the TransUnion CIBIL authority to rectify the Written off in CIBIL report. For this purpose, you can raise an online dispute in CIBIL or send a complaint letter to them.

i. Raise dispute through login to your CIBIL portal:

In this method, log in to your CIBIL Portal along with your CIBIL User ID and Password. Navigate to the “Raise a Dispute” section and change the “Written-off” status to “Clear Exiting Status” and set the Written-off Amount to “ZERO”. Then submit the dispute form. After successful submission, you will receive a dispute status, starting with P21042025….

ii. Submit a written complaint along with the evidence.

To submit a written complaint in CIBIL, visit the TransUnion CIBIL official website: https://youtu.be/GS1VGR3s9QI?si=yqo3z7OQu8V8xYiw? . Fill in the dispute form with your KYC and contact details.

Then describe your concern elaborately within 3000 characters and attach the supporting documents, such as the payment receipt, No Dues Certificate or loan account statement and your CIBIL report. Then, finally, submit the dispute. Here, you also get a Service Request Number. Save all these complaint ids for future reference.

● Email sent to CIBIL Higher Authorities:

Usually, CIBIL takes 30 days to resolve your query. In case, they fail to resolve your dispute within 30 days or you’re not satisfied with their response, then you can escalate your complaint to the CIBIL grievance authorities by sending an email to

● Contact the lender and request them to update loan status in CIBIL:

In the case of write-off loan, sometimes, it does not update automatically. Youmay have to put some extra effort to update the written off in CIBIL. That’s why, when you’re raising dispute in CIBIL, simultaneously send a request mail to the respective lender for faster resolution.

RBI new guidelines on “written off” removal from CIBIL report:

Well, now you have a clear idea of what to do if there is a Written-off status in your CIBIL report. But the big question is—can you remove the “Written-off” status entirely from your report?

If you had asked the question two-three months back, then the answer would be yes. Earlier, once the outstanding loan amount was recovered, lenders used to remove the “Written-off” status from the borrower’s credit report and leave it blank.

But now, there is a twist. Recently, RBI introduced some new credit facility statuses in the credit reporting format. According to these new rules, when a borrower clears the outstanding amount after the loan has been written off, lenders are no longer allowed to remove the “Written-off” status completely. Instead, they must now report it as “Post Write-Off” status.

Already most of the lenders have started to follow the new rule and report the loan status as “Post write off closed” in the borrower CIBIL Report.

In case of “Post Write-Off closed” be assured that the written-off amounts are zeroised. If the lender did not report properly, then raise your complaint to CIBIL and the concerned lender to remove the.

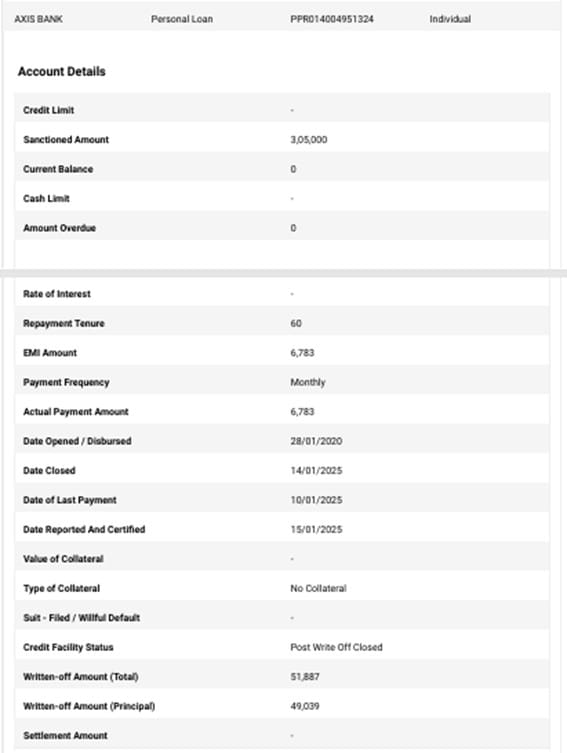

In the below credit report, we can see there was a personal loan taken from Axis Bank. The customer made default, that’s why it is reported as delinquent with overdue and written off status. However, after payment, the lender updated the loan as closed, but they changed the credit facility status from “written-off” to “Post write off closed”.

Before Payment:

After Payment:

How to deal with the new changes?

The changes are completely new for us, even for the bank managers. As a consequence, bank managers may refuse to accept your loan application due to this “Post write off closed” status in CIBIL report.

In this case, talk with the bank manager and inform them about the changes. Provide a valid reason for non-payment, in fact, you can show the no dues certificate. After all, the regulatory body, RBI, implemented these changes after considering all circumstances, so we have to accept the same.