Is there any Suit Filed status mentioned in your CIBIL report? This not only damages your credit score but also nullifies the possibility of getting further loan approval completely. Lenders will consider you a high-risk borrower and simply deny your loan application, even though you are ready to pay a high-interest rate. That’s why, if there is any suit filed present in your CIBIL report, it’s better to take some immediate action to remove the negative status; so that you can get a smooth loan approval in your financial crisis. In this article, we have discussed the different cases due to which a suit filed can be reported in a borrower’s credit report and the respective ways to remove suit filed from CIBIL report permanently.

What does a “Suit Filed” status mean in a CIBIL report and its effect on credit score?

Borrowing a loan is one of the serious financial obligations. As a responsible borrower, you have to pay your loan EMIs/ credit card bills on time. Now, what if a borrower missed his loan EMIs for a long period (for 6 months or more) intentionally or due to some financial constraint? In such cases, the lender can take legal action against the borrower to recover the unpaid debt.

Typically, when you miss your 2 to 3 EMIs repeatedly, the respective lender will notify you by sending reminder messages/ emails or over phone calls. In case you ignore all those requests continuously, after a certain period, the lender can file a petition or complaint that initiates a lawsuit against you. At the same time, they report a “Suit Filed/ Wilful Default” status to the borrower’s credit report.

The term “Suit Filed/ Wilful Default” in a loan account has a significant negative impact on the credit report, leading to a credit score drop by 80-100 points. Due to the presence of a ‘suit filed’ in your CIBIL report, obtaining any further loans from any credit institution in India will become nearly impossible.

Difference between “Suit Filed” and “Willful Default” status in CIBIL report:

Although both “Suit Filed” and “Willful Default” are terms reported on a borrower’s credit report due to legal action taken by the lender, they have slightly different meanings.

In the case of Suit Filed, it refers to the borrower who is not able to repay his loan and genuinely falls into a debt trap.

Apart from this, some borrowers have the capability and capacity to pay back the lended money to the bank. Instead of this, they used the banking system deliberately and did not pay the dues intentionally. RBI specially categorised such types of fraudsters as “wilful defaulters” and provided a strike circulation against them.

As per the RBI, a Wilful default may occur when the borrower did not repay his loan intentionally despite having sufficient funds or resources. And, if the borrower did not use the fund for the specific purpose for which the loan was sanctioned.

Does the “Suit Filed/ Wilful Default” status get removed after 7 years?

Now, a question arises, once a loan account is reported as a suit filed, how long will it remain on your CIBIL report? There is a misconception that any negative status, such as Written-off/Settled/Suit Filed, will stay on a borrower’s credit report for seven years from the first default date.However, such a practice occurs in other countries like the USA, not in India.

In USA, all the credit bureaus delete the negative information and bankruptcy from the borrower’s credit report within a time frame from 7 to 10 years.However, in India, the regulatory body RBI and all Credit Information Companies (CICs) don’t have any provisions regarding this and never promote such kind of activities. For Indian Citizens, any kind of negative remark will stay on a borrower’s credit report for life long until unless he pays the entire debt amount.

Different cases for which a “Suit Filed/ Wilful Default” status can be mentioned in a CIBIL report:

If there is any “Suit Filed/ Wilful Default” status mentioned in your CIBIL report, it does mean all times that you are a loan defaulter. Sometimes, due to the negligence of CIBIL and the lenders, a suit filed remark can be reported in your credit report, even though you are paying all of your EMIs timely. Here, we have discussed all those possibilities along with the appropriate solution.

Case 1: If the Suit Filed account is unknown to you:

As a responsible borrower, you never missed your loan EMIs or you are going to borrow for the first time. But your loan applications are rejected repeatedly and you came to know that there is a Suit filed status in your CIBIL report. After checking your CIBIL report, you noticed that the suit-filed loan account is unknown to you. You never availed of the default loan account in your life. There is a possibility that a data mixing error happened with your CIBIL report.

In case, your Name/ DOB/ Address is similar to a loan defaulter, this default loan can be reported in your CIBIL report due to the data mixing error. In this case, you can remove the entire loan account by raising a dispute in CIBIL. In addition to this, write a complaint letter in CIBIL along with your KYCs. After verification by the lender, the loan will be removed from your credit report permanently.

Case 2: The loan became Suit Filed due to non-payment:

Now, if you genuinely default on your existing loan and the account turned into suit-filed. In that case, paying the entire due is the only option to remove the suit filed from your CIBIL report. For that purpose, contact the lender and pay the entire due. After payment, raised a dispute in CIBIL to remove the Suit filed remark from the particular loan account.

Case 3: The loan is reported as Suit filed due to not being updated by the lender:

Sometimes, the record of the suit filed may still appear in your loan account even afterrepaying the debt in full. Typically, when a lender takes legal action against a loan defaulter, they initiate a court case.

Each lender maintains a separate legal department to handle such matters. After collecting the unpaid debt, the lender has to withdraw the suit file and complete all the legal process. Only after these steps are completed, the lender will update the loan status in their internal system as well as in the borrower’s credit report.

In some cases, the lender did not complete the entire process,resulting in the continued visibility of the “suit filed” remark even after paying the entire due. In such a situation, you will not get any truthful result by raising a dispute in CIBIL only. It is essential to directly contact the lender to address and resolve the issue.

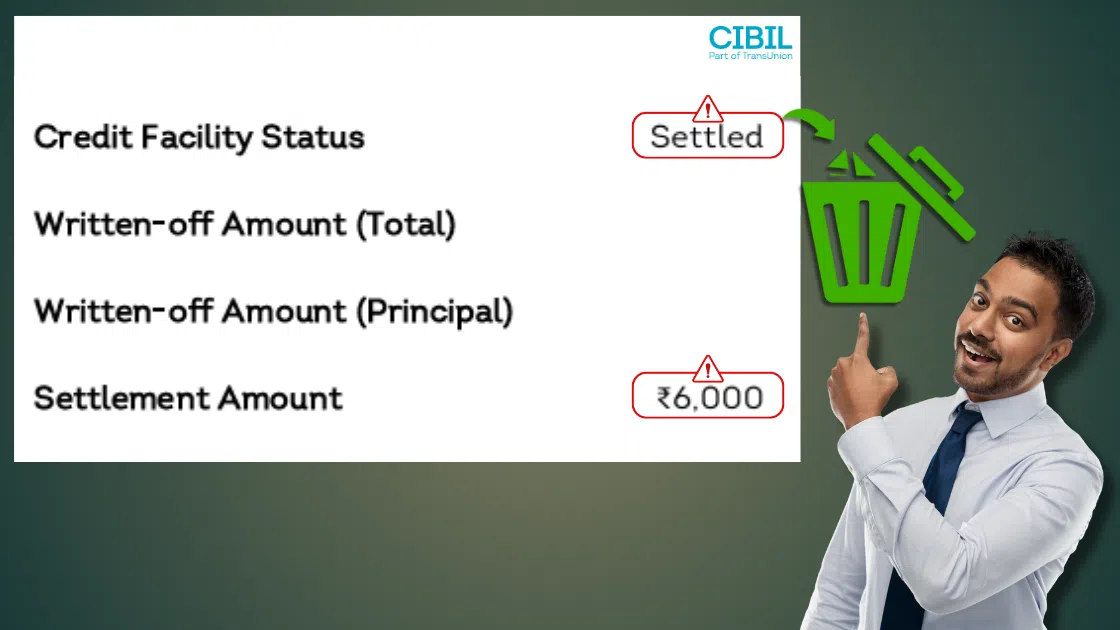

Case 4: Suit filed in a settled loan account:

When a default loan account is turned into a suit filed; the lender tries to recover the unpaid debt anyway. In many cases, the lender offers to close the loan under a compromise settlement. Typically, after a settlement, the loan status is expected to change to “Settled” rather than “Suit Filed.”

However, in certain special cases, particularly with Public Sector Undertaking (PSU) banks, the “suit filed” status may not be removed from the borrower’s CIBIL report, if the customer closes the loan through a settlement. In such instances, the borrower is required to clear the remaining outstanding balance to remove the “suit filed” remark from the loan account.

So, it is advisable to contact the lender, pay the remaining balance, and obtain a full and final payment No Dues Certificate. Subsequently, raise a dispute with CIBIL for the necessary rectification.

Steps to be followed to remove “Suit Filed/ Wilful Default” from CIBIL report:

1. Contact with the lender and pay the dues:

If any of your loan accounts turned into suit filed and the lender sent a legal notice for the same; then you should contact the lender immediately. You can visit the loan-availing branch or send an email to them for this purpose.

In case of an ongoing loan, collect the loan account statement and pay the overdue amount. After payment, you can collect the No Dues Certificate against the said loan.

If the lender requests to close the loan, then ask them to share the fore-closer/ demand letter and pay the amount as per their demand. Then, collect the loan closer letter from them.

2. Raise a dispute in CIBIL:

Now to remove the “Suit Filed” status from CIBIL, you need to raise an online dispute in TransUnion CIBIL. Change the account status to “No Suit Filed” and then submit the dispute.

In addition to this, write a complaint letter in CIBIL and request them to remove the suit filed from your loan account. And, attach your KYCs, latest CIBIL report, payment receipt, No Due Certificate, etc.

CIBIL will forward your complaint to the particular lender and after getting verification from the lender, they will remove the “Suit Filed” status from your CIBIL report.

3. Send a request to the bank:

If required, you can also send an email to the lender for a faster rectification process. Maintain a continuous follow-up with both, CIBIL & bank until the required changes are made.

Read more: